Buying and selling individual bonds can be hard. The process is slow. Prices aren’t always clear. Sometimes, it’s hard to know if you’re getting a good deal. And certain bonds, like municipal ones or bonds with special features, can be very hard to trade. Before 2010, if you wanted to build a bond ladder or plan for a future spending need, you had to buy individual bonds.

That changed in 2010 when BulletShares ETFs came out. Now it’s much easier to build bond ladders. But you might still wonder—what’s the catch? And since these ETFs are one step removed from owning the bonds yourself, do they really give you the return you expect? This article looks at the history and helps answer those questions.

What are BulletShares ETFs?

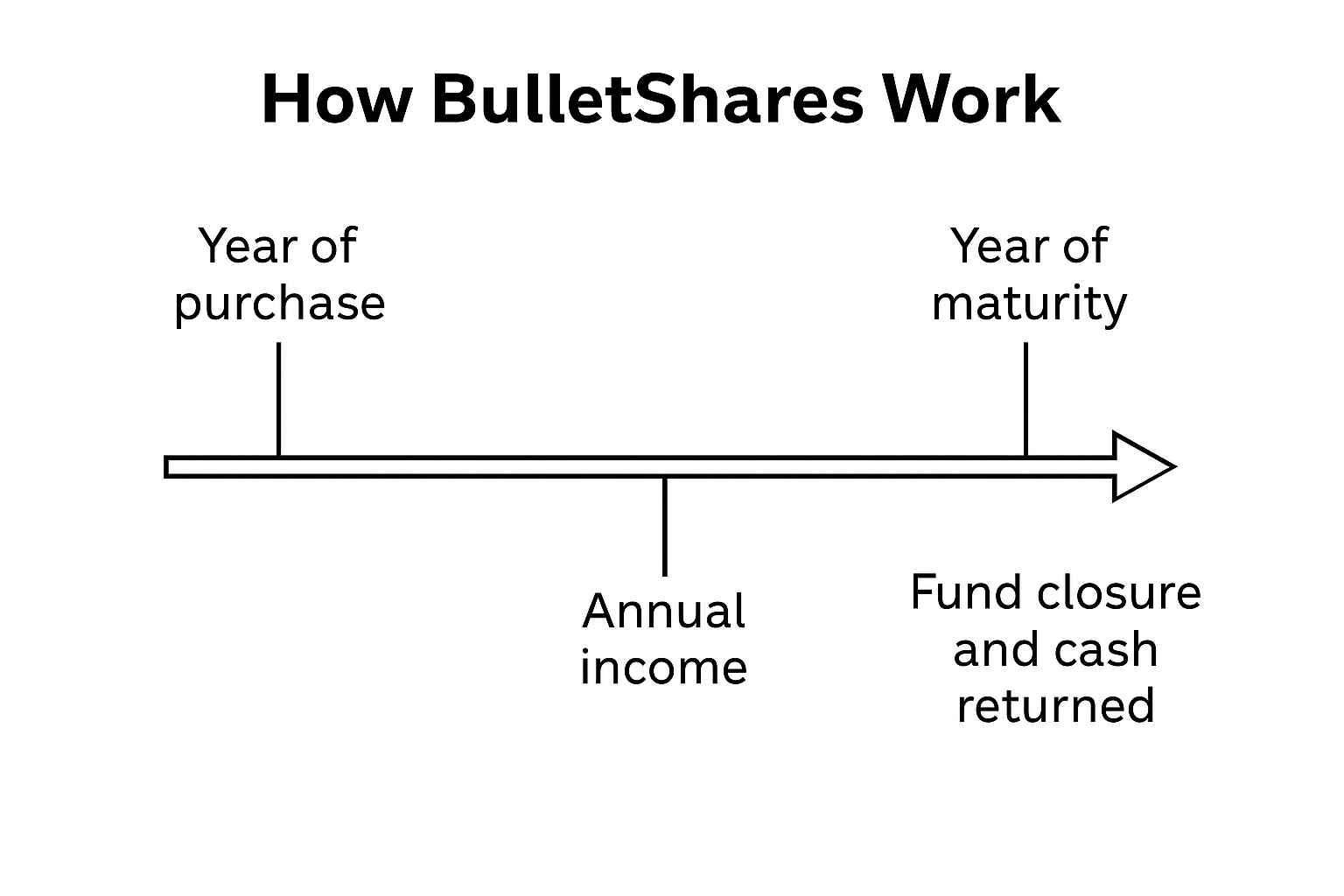

BulletShares ETFs are funds that act a lot like individual bonds. Each one holds a group of bonds that all mature in the same year. Just like a bond, each ETF has a set end date. At that time, the fund closes and returns the money to investors.

Guggenheim Investments (now part of Invesco) created the first BulletShares ETFs in 2010. BlackRock followed soon after with its iShares iBonds line. These ETFs gave investors a new way to build a bond ladder—one that was easier to manage and more flexible than buying bonds one by one.

Here’s what makes BulletShares special:

- Fixed End Date: The fund ends in a set year, like a bond.

- Diversification: The fund holds many bonds, so you’re not relying on just one or two.

- Liquidity: You can buy and sell shares easily during the day, just like with other ETFs.

Benefits of BulletShares ETFs

These funds are great for planning. If you need money in 2027, you can buy the 2027 fund. It’s hard to match that kind of timing with individual bonds.

- Diversification: The fund spreads your money across many bonds. That way, you’re less affected if one company runs into trouble.

- Liquidity: You don’t have to wait until the bond matures. You can sell your ETF shares whenever the market is open.

- Convenience: You don’t have to research or buy dozens of bonds yourself. The fund handles that for you.

- Reinvestment Options: If you want to keep your ladder growing, you can turn on automatic dividend reinvestment. That’s useful if you’re using the ETFs for short-term savings. But if you’re using them to pay for living expenses, you might want those dividends in cash. Reinvesting them might not match your goals.

Drawbacks of BulletShares ETFs

These funds aren’t perfect. Here are a few things to keep in mind:

- Fees: You pay a small fee every year to own the fund. It’s usually between 0.10% and 0.35%.

- Value at End: Unlike bonds that return the full amount (unless they default), BulletShares return the value of the fund. That might be a little more or less than the value of the bonds.

- Tracking Difference: Sometimes the fund doesn’t match the index it’s trying to follow. This difference is usually small.

BulletShares vs. Traditional Bond Ladders

Here’s how they compare:

- Flexibility: Buying individual bonds lets you control exactly which ones you own and when they mature.

- Risk Control: If you don’t like a certain company or type of bond, you can avoid it when buying directly. With an ETF, you own whatever is in the index.

- Costs: Buying bonds can cost more upfront, especially with wide bid/ask spreads. But you don’t pay yearly fees. ETFs charge a small yearly fee but are easier to manage.

| Feature | BulletShares ETF | Individual Bonds |

| Maturity Date | Fixed by fund | Fixed by bond |

| Diversification | High | Low (unless laddered) |

| Liquidity | Daily | Often limited |

| Fees | 0.10–0.35% annually | None, but higher spreads |

Conclusion

For many retirees, BulletShares ETFs offer a smart mix of control and simplicity. You lose some flexibility compared to buying bonds yourself, but you gain ease of use, good diversification, and access to your money any time. They won’t always give you exactly what an individual bond would, but they come close—and are often easier to live with.

Applications

BulletShares ETFs work well in two common situations:

- Planning for Expenses – If you know you’ll need money in a certain year (like for a car, home project, or Roth conversion), these ETFs help you set that money aside.

- Building a Bond Ladder – They’re a simple way to spread money across several years and make sure you have income when you need it.

If you’re getting ready for retirement and want steady, easy-to-manage income, BulletShares ETFs might be a good fit. Reach out to learn how a bond ladder can support your plan.

Try these next:

- Discounted Roth Conversions: What’s That Private Investment Really Worth?

- Bracket Management: The Secret Window Most Retirees Miss

- 7 Reasons to rethink a self-directed IRA (SDIRA)

- BulletShares ETFs vs. Traditional Bond Ladders: Pros and Cons for Retirees

- Are You Getting Your Money’s Worth from Morgan Stanley Private Wealth Management?