There’s a stealthy little window early in retirement—a financial lull—when your income might be the lowest it’s been in decades. But spoiler alert: it probably won’t stay that way.

Because eventually, Social Security kicks in. Required minimum distributions come knocking. And your portfolio? It could keep growing like a well-fed teenager—pushing you up the tax brackets whether you’re ready or not.

What you do (or don’t do) in this quiet phase can shape your lifetime tax bill. A 2021 study in the Journal of Financial Planning found that the difference between proactive and reactive tax planning in retirement can exceed six figures. Six. Figures. Yet most retirees sail through this low-income window like it’s just another beach day—no map, no compass, no sunscreen.

We call this game Bracket Management.

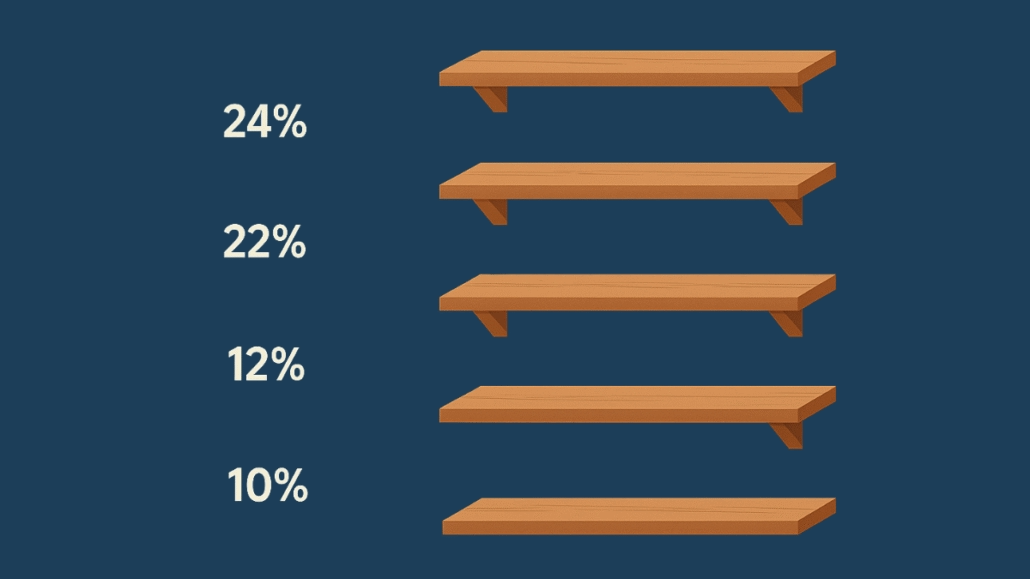

Think of your tax brackets like pantry shelves. In early retirement, many of the lower ones are sitting there empty. Bracket Management is the art of stocking those shelves intentionally—before they get jam-packed later on with surprise ingredients like Social Security and RMDs.

Say you’re married filing jointly with $40,000 of taxable income. That leaves nearly $50,000 of headroom in the 12% bracket. You could do a Roth conversion. Or withdraw a bit more for spending. Either way, you’re locking in a sweet 12% tax rate now, instead of getting clobbered by a 22% or 24% bracket later.

But here’s the twist: Bracket Management isn’t “just fill the shelf!” It’s more like Tetris than grocery shopping. Stack the wrong shape at the wrong time and suddenly—bam!—you’re triggering Medicare surcharges (IRMAA), reducing tax credits, or throwing your strategy into chaos.

It’s not “pay now vs. pay later.” It’s “pay smart, period.”

That’s why research from places like Vanguard and Morningstar consistently ranks coordinated withdrawal strategies as one of the most powerful—and underused—tools in retirement planning.

So if you’re retired or nearly there, don’t let these low-income years drift by like idle time in the waiting room. Bracket Management isn’t just tax planning—it’s tax choreography. And the sooner you start your dance, the smoother your future steps will be.