Working with Me

Why flat fees?

Have you ever found a restaurant with huge portions, great service, and prices so fair you feel conflicted leaving a glowing review—because you secretly want to keep it to yourself? That’s the kind of business I set out to build.

I’m not trying to scale a billion-dollar firm. I’m not chasing ultra-high-net-worth whales. My goal is to offer high-impact advice, priced transparently and fairly, to the people who can benefit most. You’re paying for expert service—just like when you hire a surgeon, lawyer, or CPA. You should know what that service costs, and you should be able to judge whether it’s worth it.

Flat fees create alignment. You keep 100% of your market upside. I don’t charge more just because your portfolio grew—or because you sold a business, rolled over a 401(k), or inherited real estate. I charge based on the scope of your situation, not the size of your account.

Most financial advisors still charge a percentage of your investments, which means the more you have, the more you pay—even if nothing about your situation changes. The fee grows quietly in the background, often without any clear link to the value you’re receiving. And many of those firms shy away from the tough stuff, like detailed tax planning.

Flat fees give you predictability. They remove guesswork. And most importantly, they remove conflicts. I believe advice should be based on what’s best for you—not what makes your advisor the most money.

That’s not just a pricing structure. It’s a philosophy.

Do your fees ever change?

They can, but only in ways that make sense—and never without a conversation.

Every client starts with a base flat fee that covers everything in the standard service package: retirement planning, tax strategy, investment oversight, and ongoing check-ins. If your situation calls for more—for example, if you hold a web of K-1s, private fund structures, or complex estate strategies—we’ll factor that into your quote up front. Think of it like adding extra toppings to a pizza: custom, but not a surprise.

My advisory agreements include a clause allowing for modest annual increases tied to inflation (usually based on the consumer price index). That keeps things fair and predictable. Contrast that with an AUM advisor: their fee quietly climbs every time your portfolio grows—even if their service doesn’t.

For what it’s worth, I’ve yet to raise rates for any existing client. I prefer to grow my practice by adding clients, not squeezing them.

Bottom line: you’ll never be surprised by my invoice. If your needs change, we’ll talk. And if your needs don’t change, neither will your fee.

How do I know if you’re the right fit?

If you’re between 50 and 75+, moderately tech-savvy (you can handle DocuSign and upload a PDF), and staring down retirement—or already in it—there’s a good chance we’ll get along just fine.

Most of my clients are thoughtful, capable decision makers who’ve built wealth through leadership, entrepreneurship, or specialized work in law, medicine, or real estate. They often come to me after working with a traditional AUM advisor. Often, they’ve just sold a business or property, and their fees skyrocketed. They want more than investment talk—they want a plan that speaks to taxes, timing, income, and tradeoffs.

I work best with thoughtful, capable decision-makers who want an expert partner—not a sales pitch. You likely have $2–$10 million in assets or earn over $500,000 annually, and want a specialist to help you design and execute a tax-forward retirement plan that actually makes use of the complexity you’ve built.

We’ll work together closely at first—mapping out your retirement and investment plan—then shift to a lower-touch rhythm. I visit all new clients in person during our first year, no matter where you live. I’m virtual-first, but not virtual-only.

If you want to be actively involved, appreciate straight answers, and care about tax-smart, fee-conscious advice—you’ll probably feel right at home here.

That said, I’m not the right fit for everyone. If you need handholding, resist tech, or want to pick stocks together over coffee—I’m not your person. I outsource portfolio construction to a top-tier investment committee so I can focus on what I do best: helping you make big decisions, wisely.

If that sounds like your kind of advisor, I’d love to talk.

Still unsure? Let’s talk. No pressure, just a real conversation.

What happens after I reach out?

We start with a conversation—no pressure, no pitch deck.

Our first call is about your biggest questions, your biggest risks, and whether I’m the right person to help you make sense of them. I assume you’ve read my site and watched a video or two, so I won’t waste time on small talk about my credentials. I’ll spend all the time you need clarifying anything that’s unclear.

If we agree there’s a good fit, I’ll ask for your investment statements and a bit of background via secure questionnaire. Then, I’ll prepare what I call a Retirement Readiness Brief—a customized, no-cost, 20-page preview of how I think about your situation. It flags planning gaps, highlights optimization opportunities, and gives you a taste of the rigor and clarity I bring to the table.

You’ll receive the brief as a document and we’ll schedule a follow-up call to walk through it together.

If you like what you see, I’ll send over the agreement and we’ll get started. If not, you’ll walk away with insights—and no strings attached.

Schedule your Clarity Call right here.

What do clients say after working with you?

Here’s what one client had to say on Google:

“I interviewed about a dozen wealth advisors in preparation for my transition into retirement. My wife and I are so impressed by Matt. He provides the breadth of expertise and planning that advisors charging 1%+ on AUM fees do, but he charges a flat annual fee that is significantly less. He understands the nuances of tax law in addition to his expertise in financial advising. He listens. He communicates clearly and as an expert. He is confident in his recommendations. If you’re glad I did all the work so you don’t have to, get in touch with Matt. I think you’ll be impressed.”

I couldn’t have said it better myself.

Planning & Specialties

What kind of complexity can you handle?

I work best with people whose financial lives feel like a game of 3D chess.

That might mean:

- You’re retired but still have income from rentals, consulting gigs, or RSUs that keep vesting long after you’ve stopped working full-time.

- You own property in more than one state and want to reduce taxes without spinning your wheels—or losing sleep.

- You’re juggling the needs of adult children, aging parents, and your own retirement goals (all while trying to stay sane).

- You’re converting IRAs to Roths and want to do it smartly—without triggering a tax blowup.

- You’ve built real wealth and now you’re asking: How do I protect this? How do I use it well? And how do I leave something behind that’s intentional, not accidental?

Every one of these situations comes with its own tangle of tax rules, timelines, and tradeoffs. My job is to help you navigate all of it—clearly, confidently, and without needing a PhD in tax code.

The more complex your world, the more value great planning can deliver. And if that complexity has started to feel like a burden, I’ll help turn it back into an advantage.

Do you have any specialties?

If you need an advisor who understands taxes, planning, and strategy—not just asset allocation—you’re in the right place.

I specialize in multi-year tax planning for clients with multiple income streams, real estate holdings, and private equity investments. That includes everything from retirement drawdown strategies and Roth conversion ladders to managing the tax ripple effects of K-1s, liquidity events, and inherited assets. I also offer 1031 exchange consulting as a standalone service, so it almost goes without saying: I specialize in direct and private-fund real estate ownership.

Why does niche expertise matter? Because not every advisor is fluent in the tax consequences of a DST, a charitable trust, or an RSU vesting schedule. The stakes are too high to rely on surface-level advice—especially when decisions you make today can cascade across the next two decades of your life.

If your financial life feels like a mosaic of assets, timelines, and tradeoffs, you’ll benefit from working with someone who sees the whole picture—and knows how to optimize it.

What’s your planning philosophy?

Retirement isn’t the time to make things more complex—it’s the time to make things clearer. You’ve already built something meaningful. Now it’s time to protect it and make it work for you.

My approach blends research-backed frameworks (I’m a fan of Wade Pfau, if that tells you anything) with lived experience helping people navigate high-stakes decisions. I use income optimization models, funded ratios, and retirement income style assessments to align your money with your goals.

We start with depth: the first iteration of your retirement and investment plans is detailed, thoughtful, and collaborative. I’ll bring my best thinking. You’ll bring your lived experience. Together, we’ll dial it in.

From there, we focus on the highest-impact decisions first. Optimizing and refining comes later.

It’s not about complexity for its own sake or to keep you dependent on me. It’s about clarity with purpose.

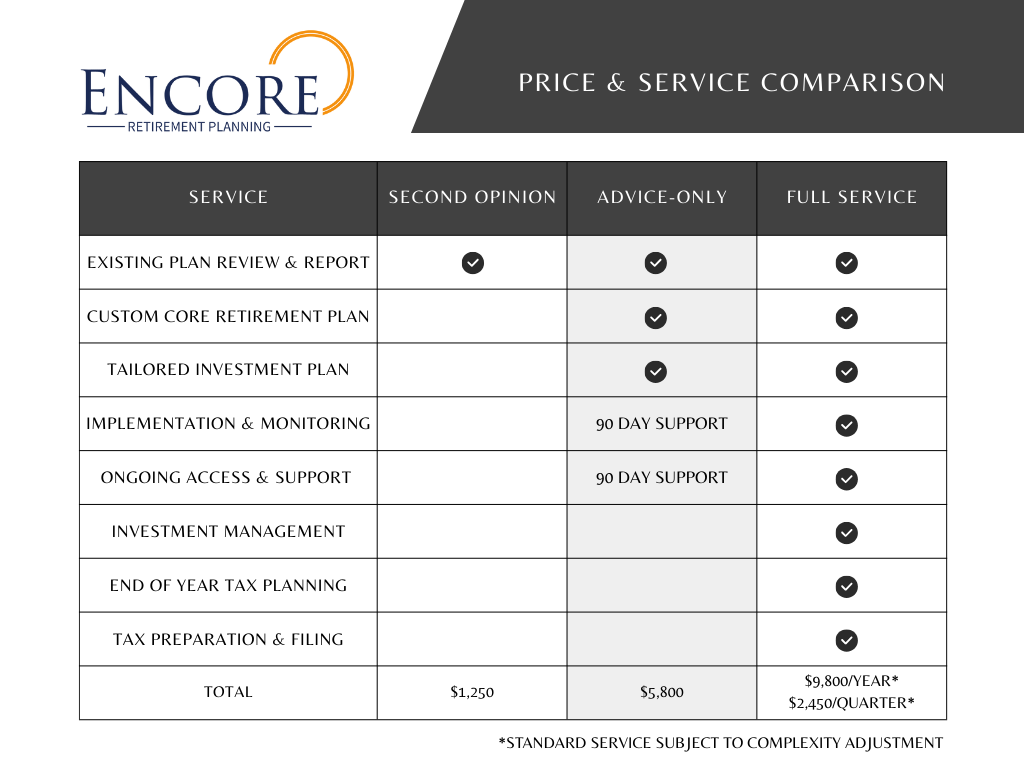

What’s included in your services?

Think of working with me like planning a flight into retirement. Some folks want a pre-flight check and flight path review. Others want help crafting a full flight plan. And some want a co-pilot in the cockpit, watching instruments, adjusting altitude, and calling out crosswinds before they hit.

Here’s how I show up at each level:

✈️ Second Opinion – The pre-flight check

You bring your existing plan and portfolio. I run diagnostics, highlight blind spots, and offer clear recommendations. You leave with a report and a briefing call—no strings attached, no long-term commitment.

🧭 Advice-Only Track – The custom flight plan

We build your plan from scratch: a tailored retirement strategy, investment plan, and tax-aware sequencing. You’ll get a full written plan, two follow-up calls, and 90 days of support while you implement it yourself.

👨✈️ Full Service – The ongoing co-pilot

You get the full flight crew: retirement planning, tax prep, investment management, estate coordination, and a strategic partner to help you course-correct along the way. We collaborate intensively up front, then shift into a steady rhythm with ongoing access, monitoring, and year-end tax planning.

Whichever service you choose, you’ll always get clear explanations, fair pricing, and advice that aligns with your altitude, speed, and destination.

Check out the pricing page for more information.

What if I just want tax prep or investment help—can I hire you for one thing?

Yes, but only if it’s the right thing.

I offer tax planning and tax prep as a standalone service through Encore Tax Services’ Personal Tax Planning package—for clients whose taxes I also file. It’s designed for people with complex income who need strategy, not just a return.

As for investment-only help: I’m not a stock picker or short-term trader. I don’t do one-off allocation advice outside the Second Opinion and Advice-Only services. But if you want your investments aligned with your retirement goals and tax plan, I’m all in.

Do you sell products?

Nope. Not unless you count clarity and confidence.

When it comes to financial products—insurance, annuities, private funds—I follow a simple rule: a product should only be introduced if it solves a real problem. If I recommend something, it’s because it’s the best tool for the job, not because I’m getting paid to push it.

I don’t take commissions, kickbacks, referral fees, or steak dinners. I’ll connect you with a vetted provider if needed, but the advice you get from me is clean and conflict-free.

Transparency & Trust

What custodian do you use?

I use Charles Schwab as my custodian.

You don’t have to move everything—just one account is enough to get started with billing and investment management. That said, most clients do end up consolidating accounts at Schwab. Why?

-

Simplicity: One login. One statement. Less mental clutter.

-

Better tools: I can use more advanced tax-sensitive strategies when I have full visibility across your accounts.

-

Cleaner planning: It’s easier to build and manage a coherent retirement strategy when everything’s in one place.

So no, you’re not required to move everything—but you might find it’s one of the smartest things you do.

What do your agreements look like?

My advisory agreement is written in plain English and designed to be as straightforward as our relationship. You’ll always know exactly what you’re signing—and why.

It’s also flexible. You can cancel anytime, no penalties, no awkward conversations. Just clear terms and mutual respect.

Here’s what the agreement includes:

- Your flat annual fee and how it’s billed (quarterly, after-the-fact)

- What’s included: investment management, tax planning, retirement strategy, and more

- Optional complexity pricing for clients with more advanced needs (private investments, complex trusts, etc.)

- A clear cancellation clause—you can walk away anytime, and any unearned fees are refunded

- A fiduciary commitment—your interests come first, always

Want to see the real thing? [Here’s a link to my current agreement.]

Spoiler: it’s shorter and friendlier than most.

Can I work with you if I already have an advisor?

Yes—especially if you’re not sure your current advisor is the right advisor.

Sometimes, people want a second opinion before making a big decision like retiring, selling property, or executing a Roth conversion strategy. Other times, they’re wondering if they’re overpaying for advice—or just not getting enough of it.

That’s why I offer a Second Opinion Service. You send over your existing plan, portfolio, and documentation, and I review it for strengths, gaps, and opportunities. You’ll get a written summary and a video call to walk through my thoughts. It’s not a new plan—it’s an audit of what you already have. And it costs less than a full engagement.

I also offer an Advice-Only Track for DIYers. That includes a comprehensive 100-page plan, two delivery meetings, and 90 days of follow-up support—all with a satisfaction guarantee.

If you want to keep your current advisor but need a sharper lens, I can help.

Are you a fiduciary? What does that really mean?

Yes. I’m a fiduciary by law and by choice.

But to me, it’s more than a label. It’s a way of operating.

I’m deeply interested in your best interest—and because I charge a flat fee, I don’t have to contort myself to pretend that what’s good for me is also good for you. There are no backdoor incentives. No soft-dollar arrangements. Just thoughtful, honest advice from someone whose success is tied to your satisfaction.