Discounted Roth Conversions: What’s That Private Investment Really Worth?

Valuation Matters More Than Ever

If you hold private investments inside a retirement account, converting them to a Roth IRA can be a powerful tax move—but only if the valuation is right.

In a Roth conversion, the value you report determines the tax you owe. When assets are hard to price, as with private placements, you have a planning opportunity—but also a risk.

This article explores how valuation intersects with Roth conversions, why the IRS pays close attention, and how to navigate the gray zones with integrity and strategy.

Who should read this:

- Investors holding private equity, real estate partnerships, or hedge funds in their IRAs

- Financial advisors helping clients with strategic Roth conversions

- Tax professionals navigating valuation complexities

Roth Conversions: A Brief Refresher

A Roth conversion involves moving assets from a pre-tax Traditional IRA into a Roth IRA. You pay ordinary income tax on the converted amount now in exchange for tax-free growth and withdrawals later.

Why convert?

- You expect to be in a higher tax bracket later

- You want to reduce required minimum distributions (RMDs)

- You want to pass tax-free assets to heirs

But when the assets involved aren’t publicly traded, valuing them fairly becomes the linchpin of a smart conversion.

The Role of Valuation in Roth Conversions

In a Roth conversion, the declared fair market value (FMV) of the asset drives the immediate tax bill. Undervalue it, and you pay less tax—but potentially invite IRS scrutiny. Overvalue it, and you give Uncle Sam more than necessary.

Bottom line: The valuation method you choose could mean thousands—or hundreds of thousands—in taxes saved or owed.

The Challenge of Valuing Private Placements

Privately held assets are notoriously difficult to value. There’s no public market price, and each investment has unique attributes that make it hard to compare.

Challenges include:

- Illiquidity

- Complex capital structures

- Lack of standardized reporting

- Conflicts of interest in sponsor-provided valuations

This makes it easy to understate value—and tempting to do so. But beware: the IRS is watching.

Common Valuation Methods (and Their Pros & Cons)

There’s no one-size-fits-all method, but these are the typical approaches:

- Cost Method: Original purchase price adjusted for impairment or appreciation. Common early on, but quickly becomes outdated.

- Market Approach: Uses comparable transactions. Rarely available with private placements.

- Income Approach: Projects future income and discounts it to today’s value. Technical but often considered more robust.

- Third-Party Appraisals: Best defense against IRS scrutiny—but expensive and not always feasible for smaller holdings.

| Method | Description | Pros | Cons | Best Use Case |

|---|---|---|---|---|

| Cost Method | Based on original purchase price, adjusted for impairment or appreciation. | Simple and often available early on. | Becomes outdated quickly; may not reflect market reality. | Early-stage investments with minimal activity. |

| Market Approach | Uses comparable transactions or assets to determine value. | Market-grounded and objective (when data exists). | Rarely applicable; hard to find true comparables. | Certain real estate or niche PE with comps. |

| Income Approach | Forecasts future income/cash flows, discounted to present value. | More accurate and accepted by IRS when done well. | Complex; requires assumptions and modeling expertise. | Mature assets with predictable cash flows. |

| Third-Party Appraisal | Independent valuation by a qualified professional. | High credibility with IRS; reduces audit risk. | Costly; may not be justified for smaller holdings. | High-value or high-risk conversions. |

What Triggers IRS Scrutiny?

The IRS tends to dig deeper when:

- Valuations appear artificially low without strong justification

- The reported value is unchanged for years despite market shifts

- There’s no third-party involvement in a sizable conversion

Audits often focus on whether the valuation reflects “fair market value”—what a willing buyer would pay a willing seller in an arm’s length transaction.

Strategic Valuation Considerations

Smart planning can reduce your tax bill while staying above board. Key strategies include:

- Timing the conversion when values are depressed (e.g., economic downturn, operational hiccups)

- Applying valuation discounts for lack of marketability or minority interest—if supported by credible methodology

- Carefully documenting the logic and assumptions behind the valuation

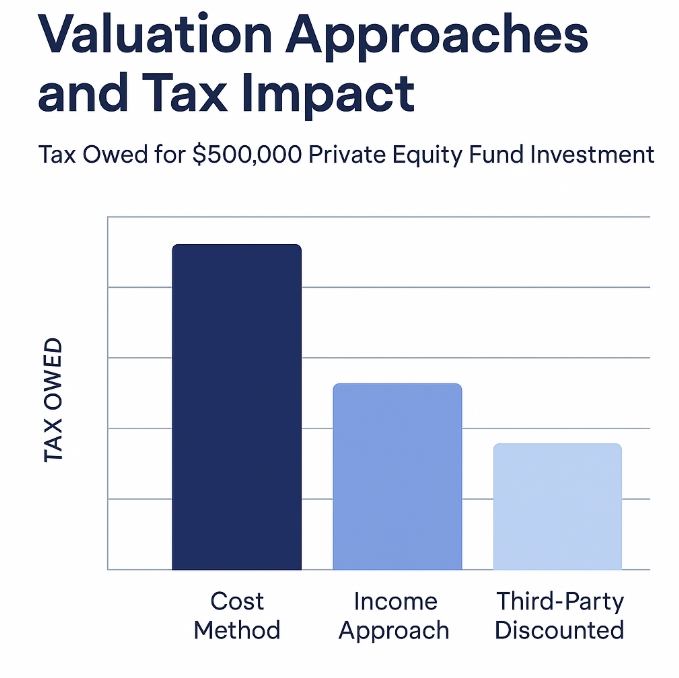

Case Study: Converting a Private Equity Fund in a Roth IRA

Imagine an investor holds a $500,000 stake in a private equity fund. The issuer reports a net asset value of $400,000 due to recent market retraction.

Using:

- The cost method: value = $500,000 → high tax bill

- The income approach: value = $375,000 → moderate tax

- A third-party valuation with discounts: value = $310,000 → potentially lowest acceptable FMV

Each method affects the tax owed, but the discounted value must be defensible or risk audit and penalties. In practice, combining a third-party report with rationale for discounts is the most bulletproof path.

Best Practices for Advisors and Investors

- Engage valuation professionals if the stakes are high

- Maintain airtight records: methodologies, assumptions, and documentation

- Stagger conversions across multiple tax years to spread out the liability

- Be transparent and conservative when uncertainty is high—penalties for missteps can be severe

Conclusion: Play It Smart—And Safe

Valuing private placements for Roth conversions sits at the intersection of tax strategy and compliance risk. It’s an area where a little sophistication goes a long way—and where cutting corners can be costly.

Takeaways:

- Private assets require special care in Roth conversions

- Valuation is both an art and a tax weapon

- Defensibility and documentation are your best allies

When done right, converting private placements at a depressed or discounted value can amplify tax-free growth and build long-term wealth. Just make sure the IRS agrees.